Executive Summary

Asia-Pacific is building the backbone of the global AI economy, but our policy discussions are focused on the wrong constraints. While water and energy use dominate headlines, fiber connectivity to billion-user markets is quietly becoming the decisive factor in where—and how profitably—AI infrastructure gets built.

This matters because it changes the post-bubble equation. When the data center investment cycle corrects, assets won’t be valued primarily by their power contracts, but by their position along fiber routes that serve Indonesia’s 283 million users, Vietnam’s 100 million, and Thailand’s 71 million.¹

The Three Factors Actually Driving Location Decisions

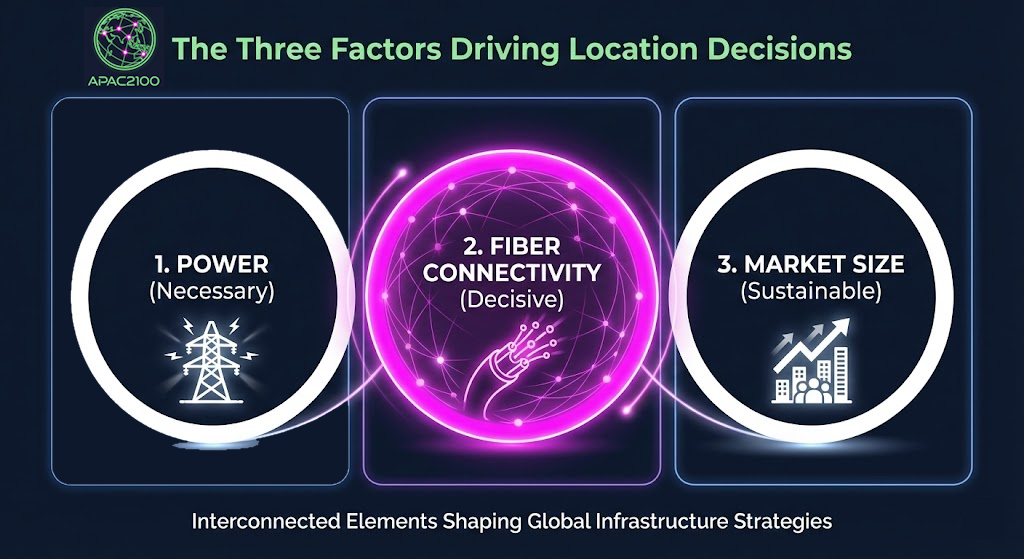

Data center developers make decisions based on an integrated calculus: power (necessary but not sufficient), fiber connectivity (determines latency and market access), and domestic market size (determines revenue sustainability).²

This explains why significant new capacity clusters in power-constrained major urban centers rather than remote renewable zones. India’s data centre industry, for example, has expanded dramatically from 350 MW in 2019 to 1030 MW in 2024, with much of this growth concentrated in markets like Mumbai that offer superior connectivity despite power challenges.³ AI training workloads require extreme density and complex infrastructure choices, creating a strong incentive to locate near major connectivity hubs and submarine cable landings—a constraint that power flexibility alone cannot overcome.⁴

Strategic Concentration and Market Dynamics

The result is strategic market concentration. The economics of submarine cables, where major trans-oceanic systems can require investments of $250-$400 million, create natural monopolies and high barriers to entry.⁵ This complex landscape, with over 559 active systems and 1,636 landings globally, is dominated by a few major players who control critical infrastructure.⁶

Long-term capital providers understand this math. Indonesia’s sovereign wealth fund INA is actively targeting data centers and digital infrastructure as key investment areas, recognizing that assets with co-located fiber rights offer superior long-term value.⁷ Similarly, state-owned carriers like Telkom Indonesia control both extensive last-mile fiber networks and interconnection rights, positioning them as key infrastructure consolidators.⁸

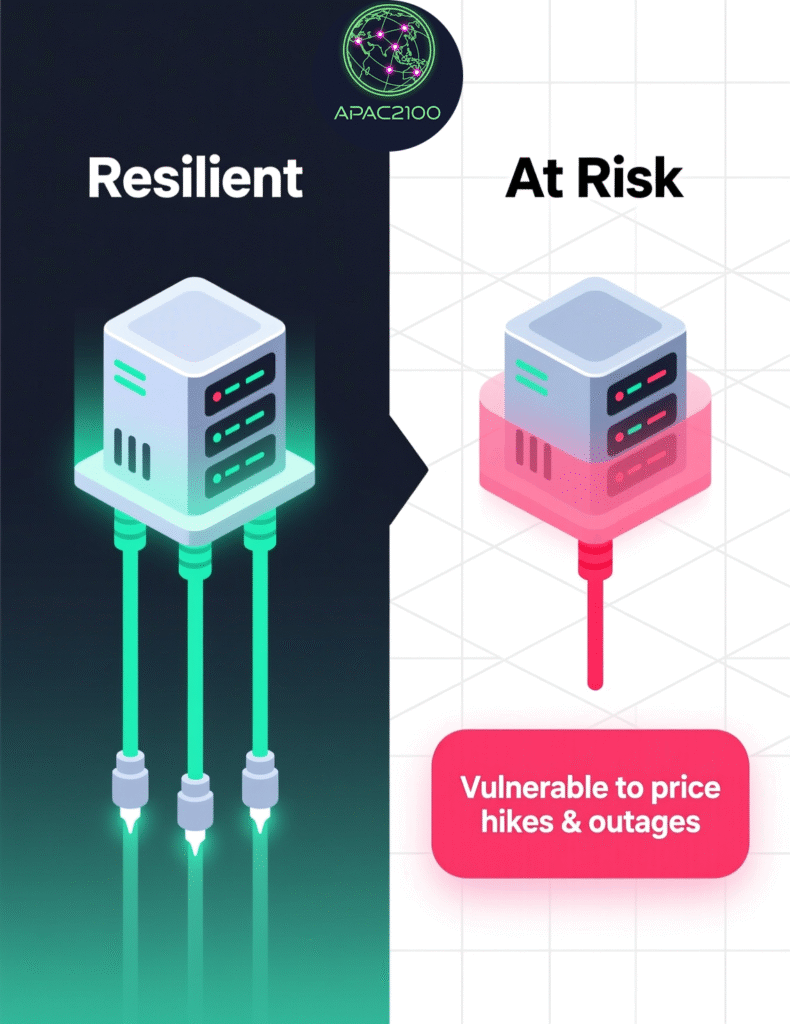

This concentration creates systemic risk. When hyperscalers face margin pressure and renegotiate leases, data centers without redundant fiber routes will be most vulnerable. Facilities with concentrated portfolios in specific markets may carry hidden exposure to connectivity bottlenecks and potential price increases from dominant fiber providers.

The Fiber-Market Disconnect

India illustrates the risk. Its robust pipeline of new data centre capacity assumes domestic AI market growth that may not materialize without proper connectivity. Developers have significantly expanded capacity near major fiber hubs, but the reliance on a limited number of providers for backhaul connectivity creates vulnerability. If fiber providers raise prices post-bubble—a likely scenario as carriers consolidate—these facilities could become economically stranded even with adequate power.⁹

Australia faces the inverse problem. Its renewable energy potential can generate compute at competitive rates, but its sparse fiber connections to Southeast Asian markets are subject to market concentration issues. The Australian Competition and Consumer Commission has identified ongoing competition concerns in the telecommunications sector, which can create barriers to reaching users efficiently.¹⁰ The power advantage can evaporate when fiber access costs create barriers to reaching regional markets.

Toward a Regional Framework

APAC needs a Fiber and Market Access Framework to align infrastructure development with sustainability goals:

- Open-access mandates: Requiring submarine cable owners to lease capacity at regulated rates, preventing vertical foreclosure. The European Union’s Open Internet Access Regulation provides a potential model for ensuring non-discriminatory access to digital infrastructure.¹¹

- Diversification requirements: Capping any single entity’s ownership of both fiber gateways and excessive compute market share.

- Resilience standards: Mandating redundant fiber routes for any facility receiving government incentives.

This ensures that when the market corrects, APAC doesn’t face a fiber-access crisis that undermines its renewable energy transition. A data center powered by geothermal energy is limited if a single cable cut isolates it from markets.

Reframing the Question

The environmental community is right to track water and energy use. But the question for APAC policymakers is: How do we ensure fiber infrastructure evolves as a shared regional commons rather than fragmented private gateways?

When assets are priced on fiber access rather than power contracts, governance matters. Getting this right today means the difference between a resilient regional grid and a system where sustainability goals are hostage to connectivity monopolies.

We must build clean—and connected.

Key Sources & Further Reading

¹ Population data: World Bank 2024 – Indonesia 283,487,931 , Vietnam 100,987,686 , Thailand 71,668,011

² Framework based on Uptime Institute’s analysis of AI workload density and data centre design requirements, 2024 : Uptime Institute Global Data Centre Survey 2024

³ India data centre capacity growth: JLL India Data Centre Market Dynamics, showing growth from 350 MW in 2019 to 1030 MW in 2024 : India’s Data Centre capacity to Reach 1.8 GW by 2027: JLL

⁴ Latency requirements: Uptime Institute, “Density choices for AI training are increasingly complex,” 2024 : Uptime Institute Global Data Centre Survey 2024

⁵ Cable cost estimates: Industry reports on submarine cable investments ranging from $250-$400 million : The Economics of Submarine Cables

⁶ Submarine cable data: TeleGeography Submarine Cable Map 2024, depicting 559 cable systems and 1,636 landings : Submarine Cable Map 2024

⁷ INA investment focus: Reuters reports on Indonesia’s sovereign wealth fund targeting data centres and digital infrastructure : Indonesia sovereign wealth fund INA targets data centres, AI in healthcare, renewables

⁸ Telkom Indonesia fiber infrastructure: Telkom Indonesia’s Infranexia solution providing extensive fiber optic coverage : Telkom Indonesia sets US$2.2b spin-off to strengthen fibre infrastructure unit

⁹ India data centre pipeline: JLL reports on India’s booming data centre industry and future projections : India’s Data Centre capacity to Reach 1.8 GW by 2027: JLL

¹⁰ Australian telecommunications market: ACCC Communications Market Report 2023-24 identifying competition concerns : ACCC Communications market report 2023-2024

¹¹ Regulatory model: European Union Regulation 2015/2120 laying down measures concerning open internet access : REGULATION (EU) 2015/2120 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL